Embedded Finance: The Hidden Growth Engine Behind Modern E-commerce

Embedded finance accounted for $2.6 trillion of U.S. financial transactions in 2021, and experts project this figure to surge beyond $7 trillion by 2026 [1]. This remarkable growth demonstrates a fundamental shift in how financial services integrate with everyday commerce.

Integrating financial services into e-commerce platforms has transformed how businesses operate and how consumers interact with digital payments. In fact, 83% of small and medium-sized businesses show interest in accessing financial services through their existing software platforms. Despite this high level of interest, only 9% currently have the capability [2].

Below, you'll find a comprehensive guide that explores how embedded finance drives e-commerce growth. You'll learn about key components, implementation strategies, and future opportunities in embedded finance. You'll also learn about successful platforms, practical implementation approaches, and ways to measure your strategy's ROI.

Understanding Embedded Finance and Why it Matters

Modern e-commerce platforms are rapidly evolving into comprehensive financial service providers. The global embedded finance market reached $82.32 billion in 2023, and it's projected to grow to $291.30 billion by 2033 [3].

What is Embedded Finance and Why it Matters

Embedded finance involves integrating financial services into non-financial platforms, making it possible for businesses to offer banking, payments, lending, and insurance services directly within their existing ecosystems. This seamless integration lets customers access financial services without leaving their preferred e-commerce platforms or apps.

Key Components of Embedded Financial Services

By integrating financial services directly into digital platforms, businesses can enhance customer experience, streamline transactions, and unlock new revenue opportunities. These capabilities enable seamless banking, payments, lending, insurance, and investment solutions, transforming the way users interact with financial products within the e-commerce ecosystem.

Core components of embedded finance in e-commerce include embedded banking, payment processing, lending solutions, insurance services and investment tools.

The Evolution of E-commerce Finance

E-commerce finance has undergone a huge transformation. The first e-commerce transaction occurred in 1994, marking the beginning of online retail [4]. The introduction of digital payment systems in the late 1990s laid the foundation for modern embedded finance solutions.

The landscape has evolved considerably since then. Plus, the rise of mobile payments and digital wallets has accelerated the adoption of embedded financial services, making it possible for businesses to offer customized lending products based on individual customer profiles [5].

Importantly, modern embedded finance solutions extend beyond basic payment processing. They now include comprehensive financial services that help reduce cart abandonment and increase customer loyalty.

This transformation has benefited small and medium-sized enterprises (SMEs) in particular. Through embedded finance solutions, these businesses can now access banking services, process payments, and offer financing options that were previously available only to larger corporations.

The Business Case for Embedded Finance

The business potential of embedded finance creates several opportunities for e-commerce platforms. Notably, embedded finance revenue is projected to increase by 148% from $92 billion in 2024 to $228 in 2028 [6].

Revenue Opportunities and Monetization Models

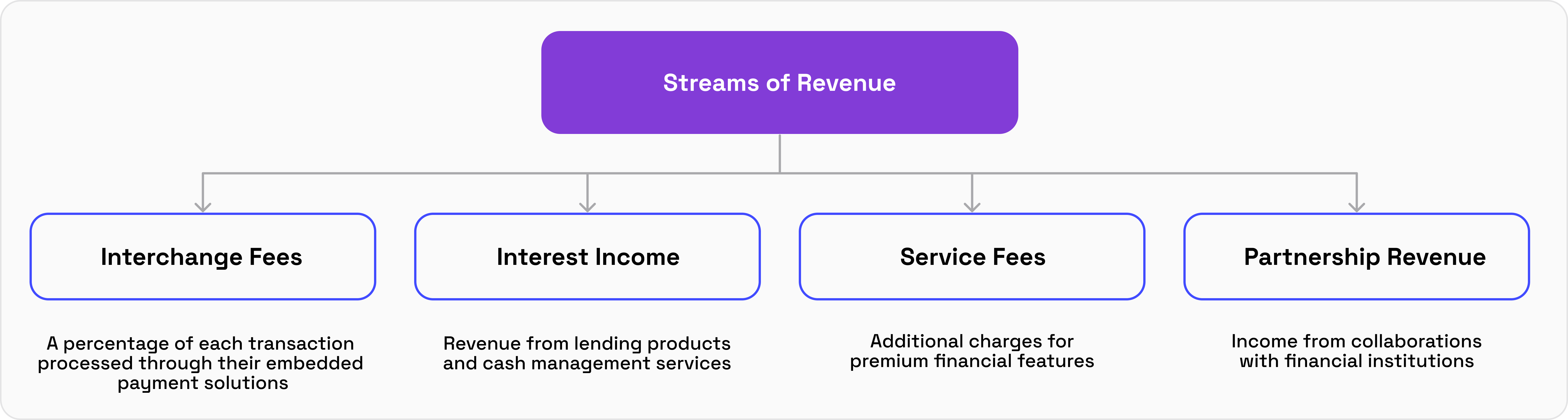

E-commerce platforms can generate revenue through multiple streams, including interchange fees, interest income, service fees, and partnership revenue.

Shopify's Merchant Solutions segment, which includes Shopify Payments, Shopify Capital, and Shopify Balance, demonstrates the revenue potential of embedded finance. In Q3 2024, Merchant Solutions generated $1.55 billion, representing 72% of Shopify's total revenue of $2.16 billion and growing 26% year-over-year [7].

Embedded finance services enable merchants to access payment processing, capital, and financial tools directly within Shopify's ecosystem, simplifying operations and boosting loyalty. The success of Merchant Solutions highlights how embedded finance can drive substantial and recurring revenue, far surpassing traditional software-only income streams.

Customer Experience Enhancement Metrics

Integrating embedded finance solutions into e-commerce platforms impacts customer satisfaction and engagement. Research indicates that 88% of businesses report increased customer engagement after they implement embedded finance solutions [8]. Specifically, platforms with embedded finance solutions see improvements in:

- Checkout conversion rates, with 20-30% higher completion rates [9]

- Average basket sizes, increasing by up to 20% through integrated financing options [9]

- Customer retention rates improving through seamless payment experiences

Cost Reduction and Operational Efficiency

Ultimately, embedded finance creates impressive operational benefits for platforms and their users. Businesses can optimize their processes and reduce expenses byintegrating financial services directly into existing workflows.

Implementing embedded finance solutions helps organizations streamline operations through:

- Automated reconciliation processes

- Reduced manual payment handling

- Simplified compliance management

- Enhanced cash flow visibility

Research shows that acquiring new customers through embedded finance channels can be 15-20 times more cost-effective than traditional methods [9]. This cost efficiency, combined with improved operational processes, helps businesses allocate resources more effectively and focus on growth initiatives.

For merchants using embedded finance solutions, the benefits extend beyond convenience. These platforms report significant reductions in payment processing costs and improved working capital management through integrated financial services [9].

Implementation Strategies for Success

Implementing embedded finance successfully requires careful planning and strategic execution. First, organizations must evaluate their readiness and choose appropriate solutions that align with their business objectives.

Assessing Organizational Readiness

Organizations need to conduct thorough assessments before integrating embedded finance into their systems. A comprehensive readiness assessment should examine:

- Technical infrastructure capabilities

- Regulatory compliance preparedness

- Resource availability- Risk management frameworks

- Customer service capabilities

Choosing the Right Embedded Finance Platforms

Choosing the right platform partner is essential for effective embedded finance. Notably, 85% of non-financial companies that offer some type of embedded finance option reported increased engagement and customer acquisition [10].

When evaluating platforms, organizations should consider:

- Technical compatibility with existing systems

- Security and compliance frameworks

- API documentation and support

- Scalability potential

- Cost structure and revenue sharing models

Building vs. Buying Considerations

The decision between building in-house solutions or partnering with established providers requires careful evaluation. Building from scratch can cost hundreds of thousands of dollars [11], while partnering with providers often requires only a small development team for integration.

Key factors that will likely influence your decision include:

- Time to Market

- Building typically takes 12-18 months

- Buying often means you can launch services within weeks or months

- Resource Requirements

- In-house development needs specialized teams

- Partnership models take advantage of existing teams

- Maintenance Considerations

- Custom solutions require ongoing updates

- Provider partnerships include maintenance support

When implementing embedded finance solutions, organizations must prioritize security and compliance, which involves robust API security protocols and following regulations like GDPR and PSD2. Through strategic partnerships, businesses can successfully integrate embedded finance while maintaining focus on their core missions.

Measuring ROI and Performance

Measuring success in embedded finance requires a structured, data-driven approach. The below guide is designed for two primary audiences: businesses adopting embedded finance solutions and financial institutions offering these solutions.

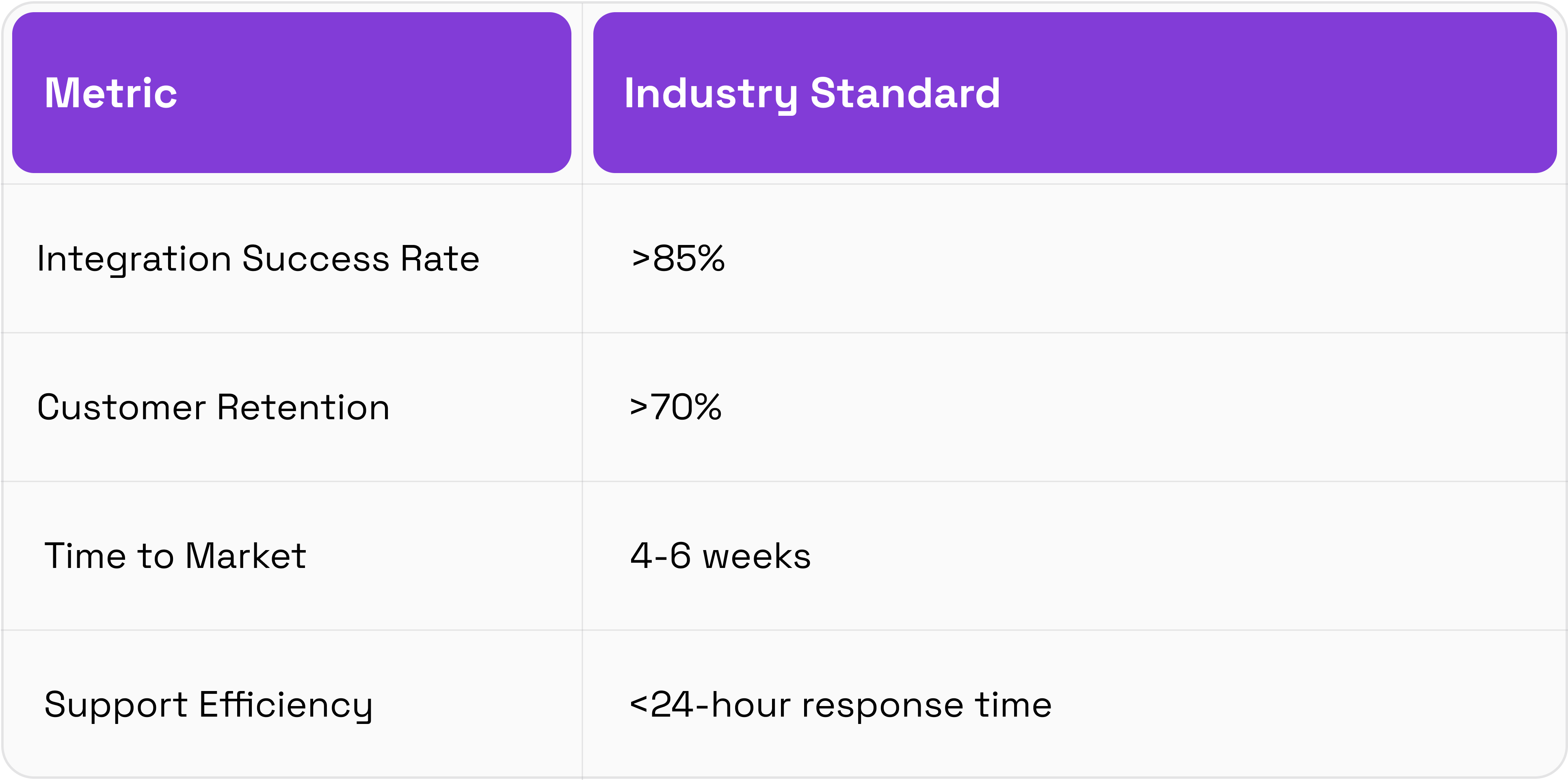

Industry Benchmarks for Performance

Comparing performance to industry standards ensures competitiveness and highlights areas for improvement. Common benchmarks include:

Demonstrating Success in Embedded Finance

For businesses, successful implementations typically lead to:

- Higher customer engagement and satisfaction

- Enhanced operational efficiency and reduced costs

- Increased revenue through better monetization of embedded solutions

- Stronger customer loyalty and lifetime value

For financial institutions, success involves delivering solutions that:

- Meet and exceed partner expectations

- Improve partner retention by providing reliable, scalable systems

- Enable deeper insights into customer behavior through embedded analytics

Continuous Improvement for Sustained Growth

Both businesses and financial institutions must continuously monitor and optimize embedded finance solutions. Organizations can ensure long-term growth and competitiveness byaligning performance metrics with business objectives and industry benchmarks.

Overcoming Common Challenges

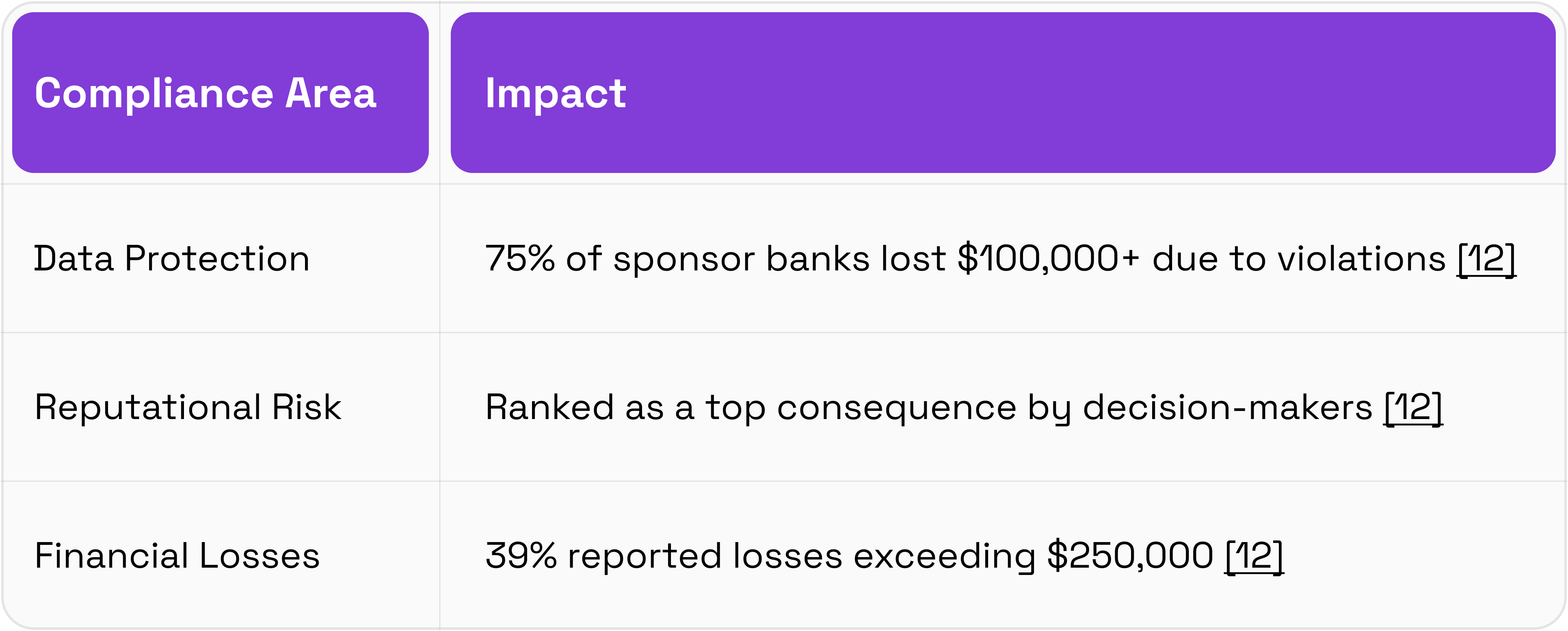

Financial institutions face mounting challenges as embedded finance reshapes the banking landscape. Recent data shows that 80% of U.S.-based sponsor banks report difficulties meeting embedded finance compliance requirements [12].

Regulatory Compliance and Risk Management

Regulatory scrutiny has intensified, with enforcement actions against fintech partner banks making up 35% of all regulatory notices in early 2024 [12]. Financial institutions must navigate a complex landscape of requirements:

Technical Integration Hurdles

Technical integration presents substantial obstacles for organizations implementing embedded finance solutions. Approximately 43% of businesses struggle with technical integration, particularly when aligning with legacy systems [13].

Notable technical challenges include:

- Complex API architecture implementation

- Security protocol establishment

- Data flow management across multiple partners

- Legacy system compatibility

Change Management and Adoption

Change management fundamentally impacts the success of embedded finance initiatives. Currently, 93% of executives report slow adoption rates as a significant challenge [13]. Organizations must address several key barriers:

- Stakeholder Education

- Communicating the benefits of embedded finance

- Demonstrating ROI potential

- Addressing security concerns

- Operational Transformation

- Updating existing processes

- Training staff on new systems

- Establishing new risk management frameworks

Successful implementation requires a comprehensive approach to risk management. Research indicates that 94% of survey respondents plan to invest in new compliance technology to manage their embedded finance partnerships [14].

To overcome these challenges, organizations are adopting innovative solutions. For instance, some banks have implemented real-time third-party risk management capabilities to ensure oversight across the value chain [15]. This lets them maintain control while encouraging innovation and growth.

The complexity of embedded finance partnerships demands enhanced governance frameworks. Data shows that 29% of respondents indicate they might discontinue their Banking as a Service or embedded finance partnerships if regulatory imbalances and associated costs persist [14].

Future Growth Opportunities

The embedded finance landscape is positioned for remarkable expansion through 2025 and beyond. The global market reached $82.70 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 21.3% from 2024 to 2033 [16].

Emerging Embedded Finance Trends

The Asia-Pacific region is poised to experience the fastest regional growth within the global embedded finance market. This swift expansion can be attributed to the high number of smartphone and internet users in countries like India, China, Indonesia, and Vietnam [17].

Key trends shaping the future include:

- Increased adoption of Banking as a Service (BaaS)

- Personalized financial services through AI integration

- Deeper integration with e-commerce platforms

- Expansion of digital wallets and buy-now-pay-later solutions

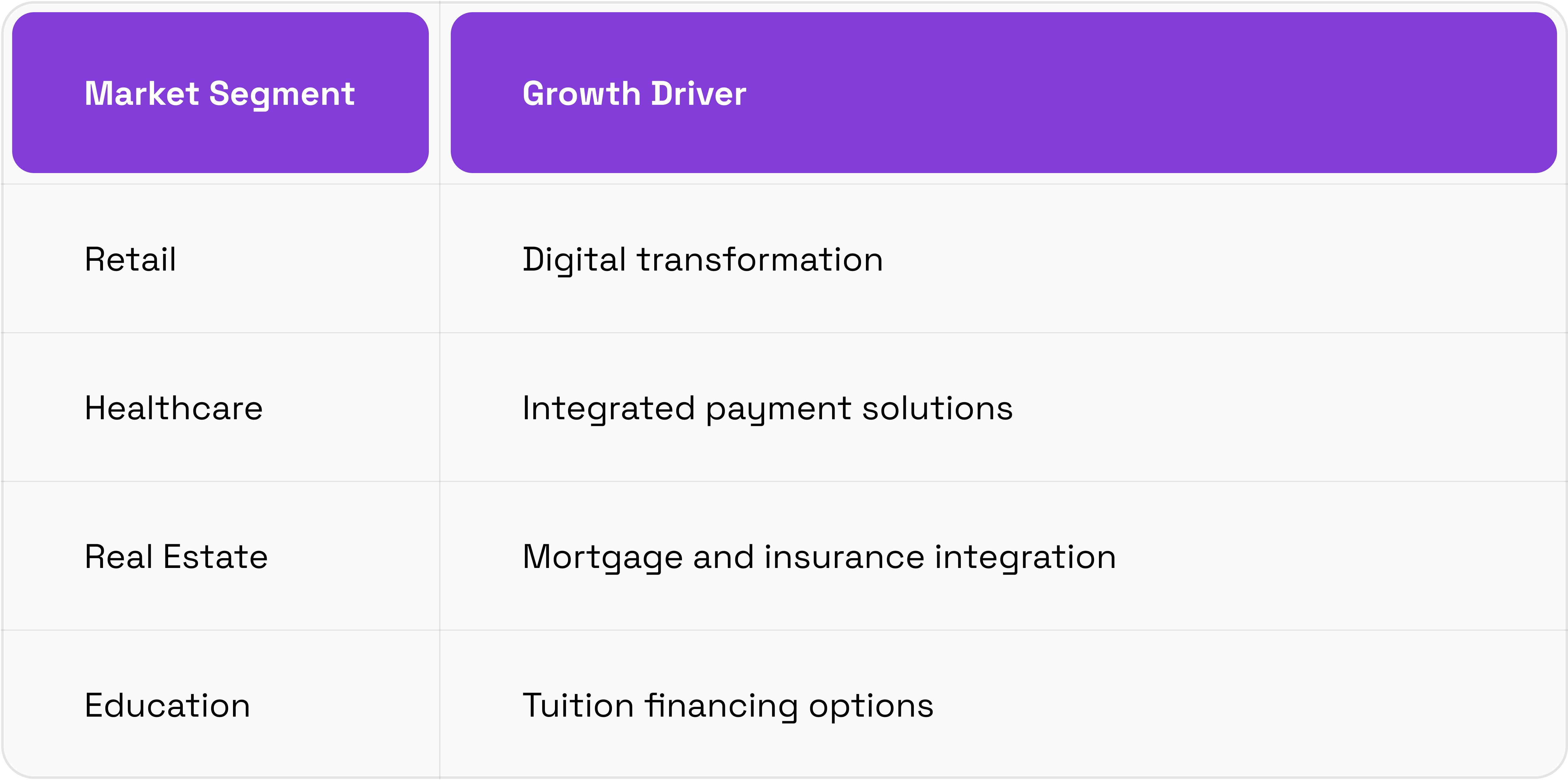

New Market Opportunities

The embedded finance sector presents substantial opportunities across various industries. In essence, the market is expected to reach $533.96 billion by 2029 [18], primarily driven by:

Above all, the embedded payment segment is projected to maintain the largest market share, driven by growing customer demand for seamless payment transactions and enhanced security [17].

Innovation Roadmap Planning

Organizations must develop comprehensive strategies to capitalize on these opportunities. The innovation roadmap encompasses several key areas:

- Technology Infrastructure

- Open banking API development

- Cloud-based solution implementation

- Advanced data analytics integration

- Strategic Partnerships

- Collaboration with fintech providers

- Integration with established financial institutions

- Cross-industry alliances

Meanwhile, regulatory developments are shaping the future landscape. The proposed financial data access (FIDA) framework and a third European Payment Services Directive will ultimately facilitate embedded finance adoption [9].

Shifting customer behaviors and advancing technology signal an even more promising path for growth. Customers increasingly desire financial services that seamlessly embed into the customer journey.

In the banking sector, embedded finance presents unique opportunities. By 2030, embedded finance channels might initiate 20-25% of retail banking sales to individuals and SMEs, increasing substantially from the current 5-10% [9].

The evolution of embedded finance solutions continues to accelerate through technological advancement. Instant connections to public data sources, such as tax records, and private sources, such as account transactions and balances, help underwriters make decisions almost instantly [9].

Looking ahead, the embedded finance ecosystem will likely see further consolidation and specialization. Organizations that can combine technological innovation with strategic partnerships will be best positioned to capture market share in this evolving landscape.

Preparing for the Future of Embedded Finance

Embedded finance is reshaping e-commerce. The projected growth from $82.32 billion to $291.30 billion signals strong market confidence in these solutions [18]. Above all, businesses implementing embedded finance report significant improvements across key metrics — from increased customer engagement to streamlined operations.

The success of embedded finance depends on careful planning, robust implementation strategies, and continuous performance monitoring. Businesses must select appropriate solutions, maintain regulatory compliance, and track essential KPIs to ensure optimal returns on their investments.

The future holds promising opportunities as emerging technologies and changing consumer preferences drive innovation in embedded finance. The Asia-Pacific region leads this growth, while sectors like retail, healthcare, and education present new possibilities for financial service integration.

Organizations will need expert guidance to navigate this evolving space effectively. Staq's team of embedded finance specialists is ready to help businesses develop and implement successful strategies tailored to their specific needs.

Embedded finance will continue transforming how businesses operate and serve their customers. Companies that embrace these solutions now position themselves at the forefront of e-commerce innovation, ready to capture the opportunities this dynamic market presents.